What you will find on this page: Does Nuclear Power have a Future in Australia? mapped – world’s coal plants (interactive map); latest on fossil fuel subsidies; countries with carbon prices; Adani myths & facts; renewable power complexity; world’s largest CO2 importers & exporters; 100 companies 71% emissions; pollution and price report; a President Trump? China’s coal war; climate change is about power (video); history of fossil fuels (video); significant fossil fuel projects; IMF not telling all; battle of the giants; oil boom or bust (video); coal seam gas; fracking what is it (videos); pros & cons of fracking; coal in Australia regional context;

Where we are and where we need to be

25 February 2016, Renew Economy, Graph of the Day: The myth about energy subsidies. Ever hear the story about why renewable energy can’t compete without a subsidy? You hear it all the time from the fossil fuel industry. And the response from renewables? Take away fossil fuel subsidies, and they’d be glad to compete on level terms. This graph below, displayed today by David Hochschild, a commissioner with the California Energy Commission, at the Energy Productivity Summer Study in Sydney, illustrates why the fossil fuel and nuclear industries don’t want that to happen. Studies by the International Energy Agency point out that global subsidies for fossil fuels outstrip those for renewable energy nearly 10-fold. The International Monetary Fund said if climate and environmental costs were included, then the fossil fuel subsides increased another 10 times to nearly $5 trillion a year.

This graph, that Hochschild sourced from DBL Investors, shows the accumulated energy subsidies in the US under federal programs. Oil and gas dominate, followed by nuclear. Federal renewable energy subsidies, in the form of investment and tax credits, are a small fraction. “The fossil fuel industry hates to talk about that,” Hochschild told RenewEconomy in an interview after his presentation. “There is a myth around subsidies, but there is no such thing as an unsubsidised unit of energy.” Read More here

This graph, that Hochschild sourced from DBL Investors, shows the accumulated energy subsidies in the US under federal programs. Oil and gas dominate, followed by nuclear. Federal renewable energy subsidies, in the form of investment and tax credits, are a small fraction. “The fossil fuel industry hates to talk about that,” Hochschild told RenewEconomy in an interview after his presentation. “There is a myth around subsidies, but there is no such thing as an unsubsidised unit of energy.” Read More here

23 February 2016, Climate Home, A flying fairy tale: Why aviation carbon cuts won’t take off. Ten days ago the airline industry stunned the world. After years of prevarication the world’s top airlines and leading manufacturers said they would take climate change seriously. The UN’s aviation body, ICAO for short, announced a carbon emissions standard that would apply to new aircraft from 2020, and to all new deliveries of in-production aircraft – current types, or minor variations on current types – as from 2028. Aircraft that don’t meet the standard will not be allowed to be produced after 2028. None of the operational aircraft currently in the fleet will be affected. The statement was widely acclaimed, notably by the US government. But will it really have any significant impact on reducing emissions? Our contention is it will not, riddled as it is with flaws. It will not be a “rigorous and challenging” standard as industry claimed, nor will it save the 650 megatonnes of CO2 emissions by 2040 that the White House proudly proclaimed. ICAO and states shaped the standard around parochial national manufacturer interests instead of the need to mitigate climate change. Aircraft designers will still face many challenges developing the next generation of airliners, but this standard will not be one of them. Beyond business as usual? New generation aircraft are generally some 10-15% more fuel efficient than those they replace. They need to be to sell. This translates to an average annual efficiency improvement of between 0.5% and 1.0%. Constant market pressures result in a continuously improving line when you plot the average fuel consumption of new aircraft types against their entry into commercial service date. Yet ICAO intends to regulate this ever improving trend with a flat (time independent) carbon standard. Even if the stringency is initially set at a level that will have an impact, its effect will quickly fade over time as market-driven improvements cut in. The maximum theoretical effect of the standard at maximum stringencies is just 1 gigatonne of CO2 between 2020-2040, while total CO2 emissions from aviation over this period will be in the order of some 31 Gtonnes, i.e. a potential saving of just 3%. Read More here

17 February 2016, Climate News Network, Carbon capture could be costly and risky. Attempts to remove carbon dioxide from the atmosphere and store it safely are all potentially costly gambles with the current technology, scientists say. There’s bad news for those who think that carbon dioxide can be removed from the atmosphere and stored deep in the Earth’s rocks. Even if carbon capture is possible, sequestration in the rocks is fraught because the gas can find multiple ways to escape, according to a report by a team from Penn State University, US, in the International Journal of Greenhouse Gas Control. Carbon dioxide is not the only greenhouse gas, but it is the one that drives global warming. It escapes from power station chimneys and motor exhausts. Back in the 18th century, the air contained 280 parts of CO2 per million, but now the level has just reached 400 parts per million. In the same period, the average global temperature has risen by 1°C and will go on rising, to make climate change an increasing hazard. Switch to renewables Last December, 195 world leaders agreed in Paris to take action aimed at containing warming to – if possible – 1.5°C. Climate scientists warn that the world must switch to solar power, wind and other renewable sources. But some think that if the exhaust emissions could be trapped and stored, humans would be able to get a bit more value from their fossil fuel investments. Others see it as the only way of avoiding 2°C of warning − the agreed international safety limit prior to the Paris climate summit. The problem is that nobody is confident that carbon can be captured on a sufficient scale. “Removal of CO2 will be expensive and is currently unproven at the scale needed – so it would be much better to reduce emissions as rapidly as possible” Some projects have been abandoned, and others suggest that the problem is that not enough has been spent on the research. But the Penn State team looked at a different aspect: whether CO2 could be buried and forgotten. So they tested laboratory reactions that involve sandstone and limestone – two of the sedimentary rocks found most often in geological strata – and water and carbon dioxide. Read More here

22 February 2016, The Conversation, Queensland land clearing is undermining Australia’s environmental progress. Land clearing has returned to Queensland in a big way. After we expressed concern that policy changes since 2012 would lead to a resurgence in clearing of native vegetation, this outcome was confirmed by government figures released late last year. It is now clear that land clearing is accelerating in Queensland. The new data confirm that 296,000 hectares of bushland was cleared in 2013-14 – three times as much as in 2008-09 – mainly for conversion to pastures. These losses do not include the well-publicised clearing permitted by the government of nearly 900 square kilometres at two properties, Olive Vale and Strathmore, which commenced in 2015. Map showing the amount of habitat for threatened species cleared between 2012 and 2014. WWF. Alarmingly, the data show that clearing in catchments that drain onto the Great Barrier Reef increased dramatically, and constituted 35% of total clearing across Queensland in 2013-14. The loss of native vegetation cover in such regions is one of the major drivers of the deteriorating water quality in the reef’s lagoon, which threatens seagrass, coral reefs, and other marine ecosystems. The increases in land clearing are across the board. They include losses of over 100,000 hectares of old-growth habitats, as well as the destruction of “high-value regrowth” – the advanced regeneration of endangered ecosystems. These ecosystems have already been reduced to less than 10% of their original extent, and their recovery relies on allowing this regrowth to mature. Alarmingly, our analysis of where the recent clearing has occurred reveals that even “of concern” and “endangered” remnant ecosystems are being lost at much higher rates now than before. Read More here

End Latest News

Does Nuclear Power have a Future in Australia?

22 March 2024, Dr Alan Finkel, The Guardian: Here’s why there is no nuclear option for Australia to reach net zero. Any call to go directly from coal to nuclear is effectively a call to delay decarbonisation of our electricity system by 20 years. The battle lines have been drawn over Australia’s energy future… Read more here

11 June 2024, ABC News: Does nuclear power have a future in Australia? These numbers will help cut through the debate s the shift away from fossil fuels gathers pace, the Coalition has turned to an emissions-free technology that has a long and contentious history — nuclear fission. To help make sense of what role, if any, nuclear power could play we turned to Alan Finkel, Australia’s former chief scientist, and economist John Quiggin. These are the numbers that you should keep in mind when thinking about its place in Australia’s energy transition. Read more here

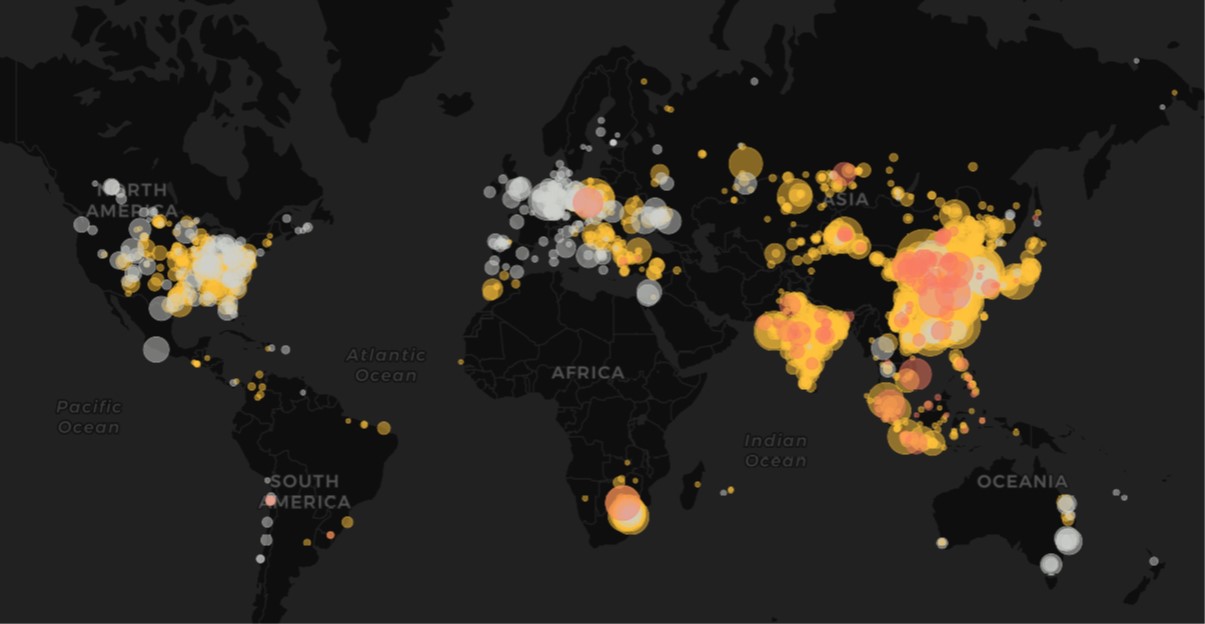

March 2019, Carbon Brief Since 2000, the world has doubled its coal-fired power capacity to around 2,000 gigawatts (GW) after explosive growth in China and India. A further 236GW is being built and 336GW is planned. More recently, 227GW has closed due to a wave of retirements across the EU and US. Combined with a rapid slowdown in the number of new plants being built, this means the number of coal units operating around the world fell for the first time in 2018, Carbon Brief analysis suggests. Another 186GW is already set to retire by 2030 and 14 of the world’s 78 coal-powered countries plan a total phaseout. Meanwhile, electricity generated from coal has plateaued since 2014, so the expanding fleet is running fewer hours than ever. This erodes coal’s bottom line, as does competition from gas and renewables. Access interactive map by clicking on image. Read more here

Click on image to go to interactive map

Latest on fossil fuel subsidies

13 May 2019, Renew Economy, Global fossil fuel subsidies reach $5.2 trillion, and $29 billion in Australia. New analysis commissioned by the International Monetary Fund has shown that global fossil fuel subsidies continue to grow, despite the growing urgency of the need to decarbonise the global economy. The working paper prepared by the IMF Fiscal Affairs Department estimated that, in 2017, global fossil fuel subsidies grew to $5.2 trillion, representing 6.5 per cent of combined global GDP. China leads all countries in the level of subsidies provided to fossil fuels, which the IMF report estimated to total $1.4 trillion in 2015. The United States followed with $649 billion in subsidies, Russia with $551 billion and the EU with $289 billion. The IMF estimates that annual energy subsidies in Australia total $29 billion, representing 2.3 per cent of Australian GDP. On a per capita basis, Australian fossil fuel subsidies amount to $1,198 per person. Australia ranked below most countries for mortality rate from pollution related illnesses, with the IMF attributing 2.6 deaths per 1,000 in Australia to local air pollution associated with fossil fuels. This is less than half the rate observed in China (5.3 deaths per 1,000) and significantly below Russia (10.0 deaths per 1,000) and the Ukraine (16.0 deaths per 1,000), where little by way of regulation exists to protect people from air pollution. The IMF found that the removal of fossil fuel subsidies would have significant economic benefits, including improved budget bottom-lines for governments. The net benefits of eliminating fossil fuel subsidies would amount to 1.7 per cent of global GDP. Read more here

20 March 2019, Desmog Global Banks, Led by JPMorgan Chase, Invested $1.9 Trillion in Fossil Fuels Since Paris Climate Pact. A report published today names the banks that have played the biggest recent role in funding fossil fuel projects, finding that since 2016, immediately following the Paris Agreement’s adoption, 33 global banks have poured $1.9 trillion into financing climate-changing projects worldwide. The top four banks that invested most heavily in fossil fuel projects are all based in the U.S., and include JPMorgan Chase, Wells Fargo, Citi, and Bank of America. Royal Bank of Canada, Barclays in Europe, Japan’s MUFG, TD Bank, Scotiabank, and Mizuho make up the remainder of the top 10. This report comes as March has already brought deadly weather to places such as the American Midwest, where historic flooding has left four dead and farm losses could reach $1 billion, and Mozambique, where Tropical Cyclone Idai has devastated the East African country and President Filipe Nyusi estimated that more than a thousand people are likely dead. Both disasters have been linked to climate change. “Increased flooding is one of the clearest signals of a changing climate,” said 350.org co-founder Bill McKibben in a statement published by ThinkProgress, adding that flooded Nebraska’s “current trauma is part of everyone’s future.” Read more here

These Countries Have Prices on Carbon. Are They Working?

April 2019, New York Times: The idea of putting a price on carbon dioxide emissions to help tackle climate change has been slowly spreading around the globe over the past two decades. This week, Canada’s federal government took the latest step when it extended its carbon-pricing program nationwide by imposing a tax on fossil fuels in four provinces that had declined to write their own climate plans. More than 40 governments worldwide have now adopted some sort of price on carbon, either through direct taxes on fossil fuels or through cap-and-trade programs. In Britain, coal use plummeted after the introduction of a carbon tax in 2013. In the Northeastern United States, nine states have set a cap on emissions from the power sector and require companies to buy tradable pollution permits. Below is their entry for Australia. Access full article here

AUSTRALIA

In 2012, Australia’s Labor Government rolled out a cap-and-trade program that essentially set a price on carbon of $23 per ton. Emissions fell nationwide under the program, but the policy faced a fierce political backlash from industry groups and voters. When the more conservative Liberal Party swept into power in 2013, it quickly repealed the program. Australia currently has a far more lenient carbon pricing program in place, called the Safeguard Mechanism, in which large industrial polluters that exceed a pollution baseline can buy carbon credits to compensate. In 2017, only a handful of companies, including several coal mines, spent about $6 millionbuying credits. Australia is currently on track to miss its overall goals for cutting emissions. Carbon pricing could still make a comeback. Australia is expected to hold federal elections in May, and the Labor Partyhas proposed bringing back a scaled-down version of cap-and-trade for the nation’s largest polluters. Still, carbon pricing remains a contentious issue in the country, which has been hit hard by global warming but is also the world’s biggest exporter of coal.

If you want a concise but precise summary of the most talked about myths and facts about the Adani proposal access this site: The Myths About Adani Jobs

World’s largest CO2 importers and exporters

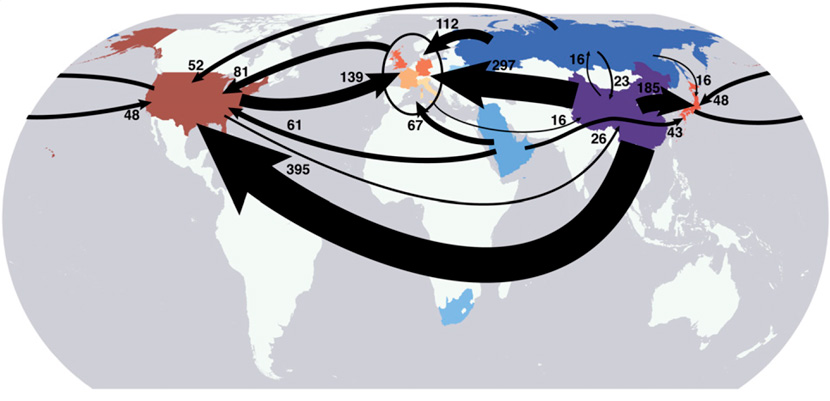

5 July 2017, Carbon Brief, Mapped: The world’s largest CO2 importers and exporters. Around 22% of global CO2 emissions stem from the production of goods that are, ultimately, consumed in a different country. However, traditional inventories do not include emissions associated with imported goods. While the US and many European countries have reduced their domestic emissions over recent decades, some of this reduction has been offset by increasing imports from countries, such as China, that have a more carbon-intensive energy mix.Even though domestic emissions have fallen 27% in the UK between 1990 and 2014, once CO2 imports from trade are considered this drops to only an 11% reduction. Similarly, a 9% increase in domestic US emissions since 1990 turns out to be a 17% increase when trade is included. Including emissions outsourced to other countries provides a more complete picture of the true responsibility associated with a country’s actions. It also accounts for carbon transfers associated with the decline of the manufacturing sector in the developed world. Carbon Brief has mapped out exports and imports of CO2 globally, and examines how including them changes countries’ national CO2 emissions. Read More here

Global emission transfers between countries in 2004 in millions of tonnes of CO2 (MtCO2), taken from Figure 1 in Davis and Caldeira 2010.

100 Companies Are to Blame for 71% of Greenhouse Gas Emissions since 1988

10 July 2017, EcoWatch, New research claims that just 100 fossil fuel producers are to blame for 71 percent of industrial greenhouse gases since 1988, the year human-induced climate change was officially recognized through the establishment of the Intergovernmental Panel on Climate Change (IPCC). Despite the landmark establishment, the oil, coal and gas industry has expanded significantly and has become even more carbon-intensive since 1988, according the 2017 Carbon Majors report from the environmental not-for-profit CDP. Here are the top 10 greenhouse gas emitters since 1988 followed by the percentage of global industrial greenhouse gas emissions, according to the Carbon Majors report:

Read More here and access full CDP Report here

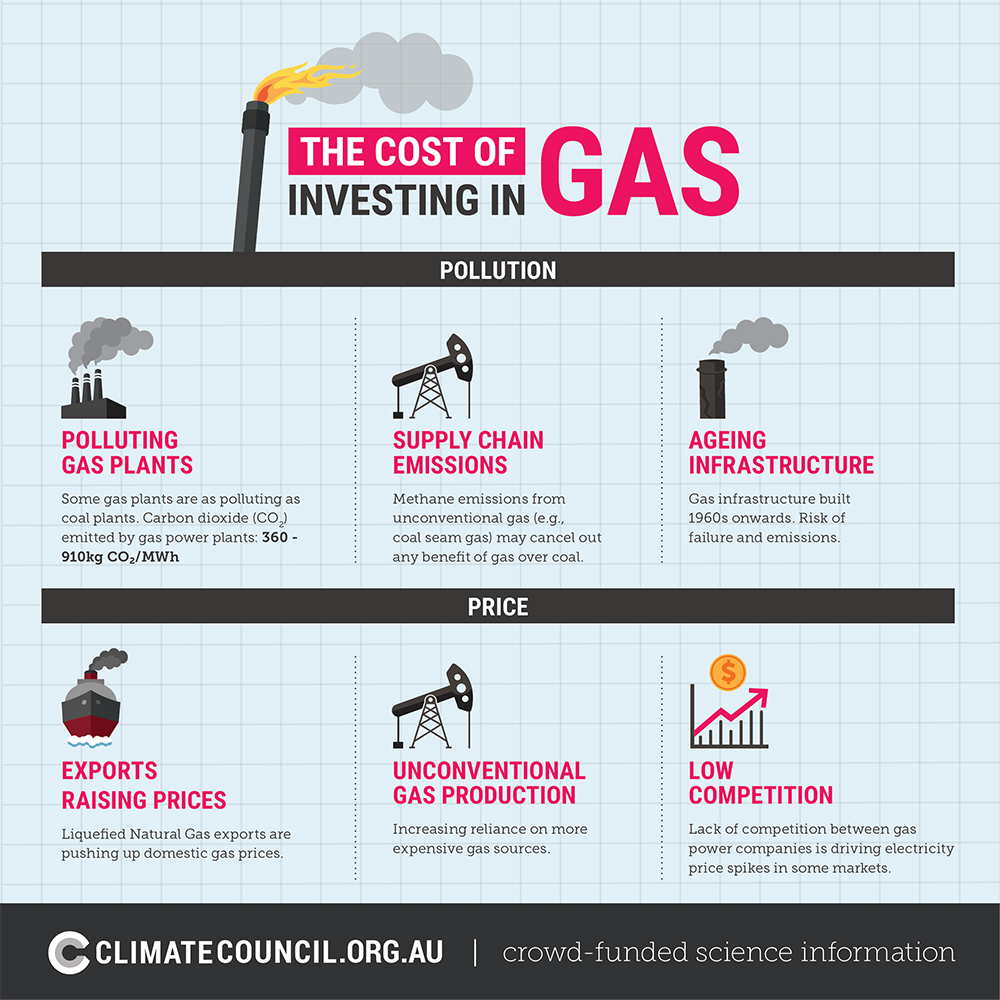

Pollution and Price: The cost of Investing in Gas

19 April 2017, Climate Council Report: Pollution and Price: The Cost of Investing in Gas.

Investing in more gas will lock in high electricity prices and pollution for decades to come. Our new report, ‘Pollution and Price: The cost of investing in gas,’ shows that tackling climate change and protecting Australians from worsening extreme weather requires our electricity system to produce zero emissions before 2050. Gas is not sufficiently less polluting than coal to garner any climate benefit. Furthermore, greater reliance on gas will drive higher power prices. While renewable energy can provide a secure, affordable alternative to new fossil fuels. Access Report here

3 August 2016, Jeremy Leggett, State of The Transition, July 2016: Might the fossil fuel industries implode faster than the clean energy industries can grow to replace them? In a memorable recent statement, some of Germany’s top scientists argued that “controlled implosion of fossil industries and explosive renewables development” can deliver the targets in the Paris agreement on climate change. Taking this premise at face value, and setting aside the thought that other factors might also be needed, the course of events in July does not offer much hope that “controlled” is a word easily applicable to the array of existential problems currently battering the energy incumbency. And while the clean energy industries continue to make progress, they are clearly not “exploding” as fast as they could. Might it be that the ongoing implosion of fossil fuel industries will happen much faster than the necessarily explosive transition to solutions? Let me start with coal. The prospects for this bankruptcy-strewn industry grew worse in July. It increasing looks as though the Chinese government’s recent retreat from coal is biting, and that the peak of Chinese coal production in 2014 is real. Prof Nick Stern and others, including Chinese collaborators, argued that we are witnessing “a turning point in the climate change battle” in this development. The latest Chinese announcement is a ban on construction of many coal projects until 2018. The air pollution driving much of their retreat is slow to abate. The same is true of India.NASA data this month showed toxic air choking a vast swathe of the subcontinent, most of it deriving from fossil fuel combustion. Facing all this, even Deutsche Bank, the most recalcitrant of the coal funders, pulled back from deals in the coal mining sector. Read More here

CSAS Earth Institute, Columbia University: Several years ago Bill McKibben contacted Dr. Hansen to ask for help in providing the scientific basis for a CO2 target of 450 ppm, as he was planning to form an organization 450.org. Dr. Hansen asked Bill to hold off while he worked on a relevant paper with several of the leading experts on the global carbon cycle and global climate. After a few months the team provided results to McKibben and within a year published a monumental paper (Target atmospheric CO2:Where should humanity aim?). Dr. Hansen and team concluded that maintaining a long-term CO2 level of 450 ppm would have highly deleterious impacts, and that a more appropriate long-term goal was 350 ppm of CO2. Subsequent fundamental work on Earth’s energy imbalance (Earth’s energy imbalance and implications) confirmed the accuracy of that estimate, inspiring McKibben to form 350.org instead of 450.org. Read More here

What damage could a President Trump do to climate change action?

6 June 2016, Politico Magazine: How Obama Is ‘Trump-Proofing’ His Climate Pact. While the GOP nominee-presumptive promises to dismantle the Paris accord, U.S. officials are rushing to secure it. And Trump’s energy czar is already hinting he may back down. n a roomful of oil and gas executives in North Dakota late last month, Donald Trump reiterated his threat to “cancel” the Paris climate agreement, insisting the way to “make America great again” is to resurrect the coal industry and drill our way to prosperity. But even if Trump is elected, taking down Paris is going to be a lot harder than he thinks. That’s certainly the view of Jonathan Pershing, President Obama’s new climate envoy, who’s rushing to Trump-proof America’s commitment to the pact—minimizing ways in which a President Trump could obstruct the global carbon reduction plan. “We’re all in. We’re moving down this road,” says Pershing, who is seated on a couch in his office at the State Department, surrounded by relics of past climate negotiations. Pershing picks one up—the original United Nations document that launched them, back in 1990—as if to emphasize just how long people like him have been working to save the planet before Trump came along. The veteran diplomat, a distant relative of Gen. John “Black Jack” Pershing of World War I fame, has been in the room for many of these talks and it’s clearly a point of pride with him. Pershing took the mantle from Todd Stern in early April and is now part of a small team of senior administration officials who are trying to cement durable regulations on climate that will survive after Obama leaves office, no matter who succeeds him. Pershing is now trying to lock in the U.S. side of the accord, which requires all nations to develop public plans detailing how they would cut carbon emissions through at least 2025. Oddly enough, Trump’s own hand-picked new energy czar, Rep. Kevin Cramer of North Dakota, agrees that his boss can do only so much damage. Cramer, in an interview with me in late May, was notably noncommittal when I asked him if Trump would simply renege on the Paris accord. He noted that Trump has said at a minimum that he’d “renegotiate” it, and he made the point that this is how Trump has approached past business negotiations, starting from an extreme position. Read More here

The real war on coal is happening in China right now

A short history of fossil fuels

Source: Post Carbon Institute’s Energy Reality site

For more background on what is happening with the oil and gas “boom” of USA visit this site Shale Bubble. Is Australia going down the same path or wanting to?

1. We really need a plan; no, lots of them: Germany has arguably accomplished more toward the transition than any other nation largely because it has a plan—the Energiewende. This plan targets a 60 percent reduction in all fossil fuel use (not just in the electricity sector) by 2050, achieving a 50 percent cut in overall energy use through efficiency in power generation (fossil fueled power plants entail huge losses), buildings, and transport. It’s not a perfect plan, in that it really should aim higher than 60 percent. But it’s better than nothing, and the effort is off to a good start. Although the United States has a stated goal of generating 20 percent of its electricity from renewable sources by 2030, it does not have an equivalent official plan. Without it, we are at a significant disadvantage…….

Level One: The “easy” stuff: Nearly everyone agrees that the easiest way to kick-start the transition would be to replace coal with solar and wind power for electricity generation. That would require building lots of panels and turbines while regulating coal out of existence. Distributed generation and storage (rooftop solar panels with home- or business-scale battery packs) will help. Replacing natural gas will be harder, because gas-fired “peaking” plants are often used to buffer the intermittency of industrial-scale wind and solar inputs to the grid (see Level Two)…….

Level Two: The harder stuff: Solar and wind technologies have a drawback: they provide energy intermittently. When they become dominant within our overall energy mix, we will have to accommodate that intermittency in various ways. We’ll need substantial amounts of grid-level energy storage as well as a major grid overhaul to get the electricity sector to 80 percent renewables (thereby replacing natural gas in electricity generation). We’ll also need to start timing our energy usage to better coincide with the availability of sunlight and wind energy. That in itself will present both technological and behavioral hurdles…….

Level Three: The really hard stuff: Doing away with the last 20 percent of our current fossil fuel consumption is going to take still more time, research, and investment—as well as much more behavioral adaptation. Just one example: we currently use enormous amounts of cement for all kinds of construction activities. Cement making requires high heat, which could theoretically be supplied by sunlight, electricity, or hydrogen—but that will entail a nearly complete redesign of the process.…..

2. It’s not all about solar and wind: These two energy resources have been the subjects of most of the discussion surrounding the renewable energy transition. Prices are falling, rates of installation are high, and there is a large potential for further growth. But, with a small number of exceptions, hydropower continues to serve as the largest source of renewable electricity.The inherent intermittency of wind and solar power will pose increasing challenges as percentage levels of penetration into overall energy markets increase. Other renewable energy sources—hydropower, geothermal, and biomass—can more readily supply controllable baseload power, but they have much less opportunity for growth….

3. We must begin pre-adapting to less energy: It is unclear how much energy will be available to society at the end of the transition: there are many variables (including rates of investment and the capabilities of renewable energy technology without fossil fuels to back them up and to power their manufacture, at least in the early stages). Nevertheless, given all the challenges involved, it would be prudent to assume that people in wealthy industrialized countries will have less energy (even taking into account efficiencies in power generation and energy usage) than they would otherwise have, assuming a continuation of historic growth trends…..

4. Consumerism is a problem, not a solution: Current policy makers see increased buying and discarding of industrial products as a solution to the problem of stagnating economies. With nearly 70 percent of the United States economy tied to consumer spending, it is easy to see why consumption is encouraged. Historically, the form of social and economic order known as consumerism largely emerged as a response to industrial overproduction—one of the causes of the Great Depression—which in turn resulted from an abundant availability of cheap fossil energy. Before and especially after the Depression and World War II, the advertising and consumer credit industries grew dramatically as a means of stoking product purchases, and politicians of all political persuasions joined the chorus urging citizens to think of themselves as “consumers,” and to take their new job description to heart…..

5. Population growth makes everything harder: A discussion of population might seem off-topic. But if energy and materials (which represent embodied energy) are likely to be more scarce in the decades ahead of us, population growth will mean even less consumption per capita. And global population is indeed growing: on a net basis (births minus deaths) we are currently adding 82 million humans to the rolls each year, a larger number than at any time in the past, even if the rate of growth is slowing……

6. Fossil fuels are too valuable to allocate solely by the market: Our analysis suggests that industrial societies will need to keep using fossil fuels for some applications until the very final stages of the energy transition—and possibly beyond, for non-energy purposes. Crucially, we will need to use fossil fuels (for the time being, anyway) for industrial processes and transportation needed to build and install renewable energy systems.We will also need to continue using fossil fuels in agriculture, manufacturing, and general transportation, until robust renewable energy-based technologies are available. This implies several problems…..

7. Equity within and between nations has to be addressed: The ability to harness energy creates wealth and confers social power. With the advent of fossil fuels came a rush of wealth and power such as the world had never before seen. Naturally, humanitarians saw this as an opportunity to spread wealth and power around so as to lift all of humanity above drudgery, eliminate hunger, and even put an end to war. And to a large degree that opportunity has been seized: overall, child mortality rates are down, life expectancy is up, infectious diseases are on the decline, hunger has been reduced (even as population has dramatically grown), and mortality from violence has declined since the end of World War II…..

8. Everything is connected: Throughout the energy transition, great attention will have to be given to the interdependent linkages and supply chains connecting various sectors (communications, mining, and transport knit together most of what we do in industrial societies). Some links in supply chains will be hard to substitute, and chains can be brittle: a problem with even one link can imperil the entire chain. This is the modern manifestation of the old nursery rhyme, “for the want of a nail…the kingdom was lost.”…..

9. This is not plug-and-play; it is civilization reboot: Energy transitions change everything. From a public relations standpoint, it may be helpful to give politicians or the general public the impression that life will go on as before while we unplug coal power plants and plug in solar panels, but the reality will probably be quite different. During historic energy transitions, economies and political systems underwent profound metamorphoses. There is no reason to suppose that it will be different this time around. If this is done right, the changes that must take place will bring with them opportunities for societal improvement and the greater wellbeing of everyone—including the rest of the biosphere……

Significant fossil fuel projects that are still happening

The Guardian as part of their “Keep it in the Ground” campaign are producing a series on global “carbon bombs”. The carbon bombs are 14 giant proposed fossil fuel projects around the world that, if they go ahead, will lead to the emission of 6.3 gigatonnes of carbon dioxide a year by 2020. The stories will be listed below as they are published.

FIRST STORY – Galilee Basin Australia: Their Australia environment specialist Oliver Milman visits the Galilee basin in Queensland. The story unfolds….The plans here are truly colossal. Developers hope to establish a series of mines to exploit a deposit of 247,000 sq km (95,400 sq miles) of coal, a land mass the size of Britain. If the complex is fully developed, greenhouse gas emissions from the burned coal would top 700m tonnes a year. That would mean a CO2 output just behind Germany. There are also concerns that project will also impact the Great Barrier Reef because of the risks posed by increasing shipping to export the coal. We have established that the Australian government has engaged in a frantic diplomatic push to avoid the Great Barrier Reef being listed as “in danger” by the UN. Preventing the Galilee basin coal mines and other projects from going ahead is the front line of efforts to Keep it in the Ground and prevent dangerous climate change. Read More here

SECOND STORY – Schlumberger: Is a company with a huge £114m investment from the Wellcome Trust. The Gates Foundation Trust also holds a shareholding of more than $3m in the company. Schlumberger is ubiquitous in fossil fuel operations across the world, it employs more than 100,000 people finding, scoping, and drilling as much oil and gas as possible from 85 countries across the world. With revenues of $48bn (£30bn) a year and a valuation in excess of $116bn (£75bn), it has more staff than Google, turns over more than Goldman Sachs, and is worth more than McDonald’s – yet you won’t have heard of it. Meet the oil world’s most secretive operator. Read More here

THIRD STORY – Peabody: The truth behind Peabody’s campaign to rebrand coal as a poverty cure. The world’s largest privately-held coal company has a long history of attacking climate science. Now it is working to change the conversation from a climate crisis to one of global poverty – with coal as the solution….. Peabody’s links to the parallel universe of the climate denial movement stretch back to the early 1990s when Fred Palmer, who is now Peabody’s main lobbyist as vice-president of government affairs, founded the Greening Earth Society, an industry front group. It actively promoted the notion that climate change was a net positive, with benefits for plants and public health. Read More here

FOURTH STORY – Shell: The real story behind Shell’s climate change rhetoric. An investigation into the Shell business shows that under its forecasts the Earth’s temperature will rise nearly twice as much as the 2C threshold for dangerous climate change, and that the firm’s own greenhouse gas emissions are still rising and will rocket further after the £47bn acquisition of rival BG Group. Further, Shell’s Canadian tar sands, Brazilian, Nigerian and US Gulf deep-water projects are the most likely to be rendered worthless by a global clampdown on high carbon-emitting exploration projects, analyses find. In addition, the company’s growth is becoming reliant on drilling wells (some deeper than the one that caused BP’s Gulf blowout) and it is a member of the American Legislative Exchange Council, a political organisation that has opposed policies to address climate change. Read More here

22 May 2015, Energy Post: Why Shell can’t quite the Arctic: Despite the damage to its reputation, Shell insists on continuing its controversial Arctic campaign. The company says that the world needs the oil and gas resources of the Arctic. But according to Energy Post’s editor-in-chief Karel Beckman, it’s really Shell itself that needs those resources. Shell’s annual shareholders meeting last Tuesday (19 May) in The Hague seemed almost like a climate conference, some observers reported. Activist shareholders lined up to ask Shell to embrace the energy transition. Read More here

29 May 2015, The Guardian, Shell’s CEO, Ben Van Beurden, has agreed to be grilled by the Guardian on everything from divestment to economics and responsibility – but will he give some unguarded answers? In this extended interview, the Guardian’s editor in chief, Alan Rusbridger, head of environment Damian Carrington and energy editor Terry Macalister put all the questions you’ve wanted to ask to the head of Shell. Why do they continue to invest in new ways to take oil and gas out of the ground when they already have more than they can possibly burn? To listen to the interview go here

FIFTH STORY – BP: Revealed: BP’s close ties with the UK government. Documents show the extent of BP’s influence on government policy and how their intimate relationship is at odds with UK commitments to reduce carbon emissions. For the oil multinational BP, it was a historic moment – the signing of a joint venture to exploit the vast oil and gas reserves of Russia’s Arctic shelf with the Russian energy giant Rosneft. The deal was worth £10bn in share swaps. The chief executive of Rosneft, Igor Sechin – then Russian deputy prime minister, key Putin ally and one of the most forbidding characters in the world of oil – would be coming to London to seal the agreement. Rosneft is majority owned by the Russian state, and BP urgently needed a senior British government figure to mark the alliance. Read More here

SIXTH STORY – Tar Sands Alberta: The tar sands here are one of the single biggest source sites of the carbon pollution that is choking the planet. Mine out all the thick black petroleum, as the Canadian government proposes, ship it out by proposed pipelines such as the Keystone XL and oil trains, and abandon all hope of avoiding a climate catastrophe. Within a 25-mile radius of Fort McKay, 21 projects with a capacity of up to 3.3m barrels a day have been approved or are in production. Another 20 with a combined capacity of about 1.6m barrels a day are in the planning stage, according to Fort McKay First Nation. Locals can hear, smell, feel and taste the evidence of extraction, even inside their homes. On bad days, it smells like cat piss, according to Cece Fitzpatrick. Read More here

SEVENTH STORY – China: Chinese miners last year dug up 3.87bn tonnes of coal, more than enough to keep all four of the next largest users – the United States, India, the European Union and Russia – supplied for a year. The country is grappling with the direct costs of that coal, in miners’ lives, crippling air pollution, expanding deserts and “environmental refugees”. Desire for change contends with fears that cutting back on familiar technology could dent employment or slow growth, and efforts to cut consumption do not always mean a clampdown on mining….Although it overtook the US nearly a decade ago to become the biggest emitter of greenhouse gases, per person it still produces barely a third as much carbon dioxide as the US and half Russian levels.

The problem for those fighting to keep global warming within 2C though, is that Chinese demand has expanded so fast that anything short of a dramatic cut in coal use – something no one is even advocating – leaves terrifying amounts of carbon dioxide pumping into the atmosphere. Read More here

EIGHTH STORY – Arctic: A last great unprotected wilderness, safe haven for endangered species and home to native people whose subsistence lifestyle has survived in harmony with nature for thousands of years. It is here that Shell plans to drill for oil, pulling the detonator on a carbon bomb which eventually could spray 150bn tonnes of carbon dioxide into the atmosphere. The irony is that the drilling is only possible because manmade climate change is already causing this region to grow warmer twice as fast as the rest of the planet. The melting ice makes these huge reserves of oil and gas more accessible. It could set major oil companies against each other but also superpower against superpower as they scramble to exploit the last untapped giant reserves in a part of the world where territorial boundaries remain unclear. No wonder some fear a new cold war. Read More here

25 May 2015, Energy Post:The IMF just destroyed the main argument against clean energy. A new report by the International Monetary Fund (IMF) finds that energy (fossil fuel) subsidies are “big and rising”. At the presentation of the report, Vitor Gaspar, Director Fiscal Affairs Department at the IMF, noted that most subsidies go to coal and said the numbers were “shocking”. He added that “eliminating energy subsidies can generate substantial environmental, fiscal and welfare benefits”. Elias Hinckley, strategic adviser at the US law firm Sullivan and Worcester, argues that the IMF report can “re-write the fundamentals of the discussion about our energy future”. Read More here

Adding to the story: 21 May 2015, Richard Heinberg’s Museletter 276: IMF Tells a Half-Truth: This month’s Museletter starts out with my take on the contradictions behind the IMF’s new exposé on the extent of Global Energy Subsidies. Read More here

Battle between fossil fuel giants

Carbon Tracker Initiative – A team of financial, energy and legal experts with a ground breaking approach to limiting future greenhouse gas emissions. They are doing this using a new language and framework that approaches climate change not as something happening “out there” but something that will affect everyone financially. Resources (includes Carbon Reporting links); News; Reports; Blog

The Contest: lines being drawn

The CEOs of the European oil giants Shell, BP, Total, Statoil, Eni and BG Group, with a combined revenue of $US1.4 trillion – although notably not the US giants Chevron and Exxon – sent letters last Friday to the head of the UN climate negotiations, Christiana Figueres, and Laurent Fabius, France’s Foreign Affairs and International Development Minister who will also lead the Paris climate talks later this year. Read More here

The reality

5 June 2015, Energy Post, IEA sees “harsh reality” for gas industry: From a Golden Age of Gas to a “harsh reality” in just a few years – the 2015 “Gas medium-term market report“ released by the International Energy Agency (IEA) on 4 June in Paris sounded a warning note to anyone who believes gas is bound to conquer the world. That can still happen – but only if gas drastically improves its competitiveness, said the IEA. The IEA’s Executive Director Maria van der Hoeven and her team presented the IEA’s annual gas market report in the lion’s den, at the World Gas Conference in Paris where the prevailing mood was one of optimism about the prospects of gas. The IEA, which itself introduced the notion of a ‘Golden Age of Gas’ some years ago, now notes that the future is still quite uncertain. Above all, the most important growth market, Asia, can no longer be counted on as a certainty, said Van der Hoeven: “The belief that Asia will take whatever quantity of gas at whatever price is no longer a given.” Read More here

Source: Post Carbon Institute’s Energy Reality site

21 January 2015, Post Carbon Institute (Richard Heinberg) Our Renewable Future, Or, What I’ve Learned in 12 Years Writing about Energy. Folks who pay attention to energy and climate issues are regularly treated to two competing depictions of society’s energy options.* On one hand, the fossil fuel industry claims that its products deliver unique economic benefits, and that giving up coal, oil, and natural gas in favor of renewable energy sources like solar and wind will entail sacrifice and suffering (this gives a flavor of their argument). Saving the climate may not be worth the trouble, they say, unless we can find affordable ways to capture and sequester carbon as we continue burning fossil fuels. On the other hand, at least some renewable energy proponents tell us there is plenty of wind and sun, the fuel is free, and the only thing standing between us and a climate-protected world of plentiful, sustainable, “green” energy, jobs, and economic growth is the political clout of the coal, oil, and gas industries (here is a taste of that line of thought). Which message is right? Will our energy future be fueled by fossils (with or without carbon capture technology), or powered by abundant, renewable wind and sunlight? Does the truth lie somewhere between these extremes—that is, does an “all of the above” energy future await us? Or is our energy destiny located in a Terra Incognita that neither fossil fuel promoters nor renewable energy advocates talk much about? As maddening as it may be, the latter conclusion may be the one best supported by the facts. If that uncharted land had a motto, it might be, “How we use energy is as important as how we get it.” Read more here

REALITY CHECK: Only about 22% of global energy is consumed in the form of electrical power. Our biggest single energy source is oil, which fuels nearly all transportation. Transport is central to trade, which in turn is the beating heart of the global market economy. Oil also fuels the agricultural sector, and eating is fairly important to most of us. Of the three main fossil fuels, oil is showing the most immediate signs of depletion, and renewable options for replacing it are fairly dismal.

12 March 2013, SBS, Factbox: Here are some key facts on coal seam gas: how big is it in Australia and what are its potential environmental impacts?

WHAT IS COAL SEAM GAS? Coal seam gas is methane formed from the decay of organic matter over time, formed in the same way as coal and oil. Methane is held within the coal seam by water pressure in the seam. Extracting the gas requires depressurising the coal seam by removing the water, and may include other techniques to increase the permeability of the seam.

DIFFERENCE BETWEEN CSG AND SHALE GAS

Shale gas and coal seam gas are often confused one with one another. Shale gas is methane held within shale layers, rather than a coal seam. Shale is much harder than coal and always requires fracturing (‘fracking’) to allow the gas to flow. There is currently no shale gas production in Australia, although there are large shale gas reserves in SA, the NT and WA. In the US, shale gas supplies 15 per cent of gas consumption.

WHAT’S DRIVING THE DEMAND OF CSG IN AUSTRALIA? CSG accounts for 27 per cent of Australian gas reserves: it is set to supply at least 30 per cent of the whole nation’s domestic market by 2030, and 50 per cent of gas demand in eastern Australia. All CSG reserves are in NSW and Queensland. In the ‘Eastern Gas Market’ (NSW, Queensland, Victoria, SA, Tasmania), CSG makes up 78 per cent of gas reserves.

According to the Australian Energy Regulator, assuming that gas use keeps increasing at the current rate of 4 per cent per year until 2025, conventional gas in the Eastern Gas Market will last for nine years, while CSG will last for 27 years. As shown in this ABARE map, the Eastern Gas Market is not connected to the Western Market (WA) and the Northern Market (NT) by pipelines.

CSG EXTRACTION TECHNIQUES: Extracting CSG involves drilling a vertical well down to the coal seam and pumping out the water held in the seam. This reduces the pressure in the coal seam and allows the gas to be released. Horizontal or angled wells can also be drilled to reach the coal seam. If the flow of gas is insufficient, the coal seam gas may be fractured (‘fracked’) to increase the permeability of the coal and allow the gas to flow more freely. Read More here

Source: Fracking explained: opportunity or danger: Kurz Gesagt – In a Nutshell

Source: Sierra Club Beyond Natural Gas Campaign

The following video is how the oil/gas industry in the US presents fracking Source: Western Energy Alliance. Western Energy Alliance focuses on federal legislative, regulatory, environmental, public lands and other policy issues. They represent the voice of the Western oil and natural gas industry in a variety of ways.

27 May 2015, Yale Climate Connections, Pros and Cons of Fracking: 5 Key Issues, Have you been asked if you support or oppose fracking? A brief guide to sorting out the plusses and minuses of key fracking issues. There’s an issue where the underlying science remains a political football, and scientists are regularly challenged and called out personally. Where energy needs and short-term economic growth are set against our children’s health and future. Where the consequences of bad, short-sighted decisions may be borne primarily by a small subset of under-served and undeserving persons. And where the very descriptive terms in the debate are radioactive, words spun as epithets. We’re not talking here about global warming, and “deniers” versus “warmists.” We’re talking about the game-changing new set of unconventional oil and gas extraction technologies and techniques collectively known as hydraulic fracturing, or “fracking.

July 2015, Post Carbon Institute: Shale Gas Reality Check: Revisiting the U.S. Department of Energy Play-by-Play Forecasts through 2040 from Annual Energy Outlook 2015: In October 2014, Post Carbon Institute published the results of what likely remains the most thorough independent analysis of U.S. shale gas and tight oil production ever conducted. The process of drilling for shale gas and tight oil is known colloquially as “fracking” and has drawn a great deal of controversy—considered by some as an energy revolution and others as an environmental and human health catastrophe. Much of the cost-benefit debate over fracking has come down to the perception of just how much domestic oil and gas it can produce and at what cost. To answer this question, policymakers, the media, and the general public have typically turned to the U.S. Department of Energy’s Energy Information Administration (EIA), which every year publishes its Annual Energy Outlook (AEO).

July 2015, Post Carbon Institute: Shale Gas Reality Check: Revisiting the U.S. Department of Energy Play-by-Play Forecasts through 2040 from Annual Energy Outlook 2015: In October 2014, Post Carbon Institute published the results of what likely remains the most thorough independent analysis of U.S. shale gas and tight oil production ever conducted. The process of drilling for shale gas and tight oil is known colloquially as “fracking” and has drawn a great deal of controversy—considered by some as an energy revolution and others as an environmental and human health catastrophe. Much of the cost-benefit debate over fracking has come down to the perception of just how much domestic oil and gas it can produce and at what cost. To answer this question, policymakers, the media, and the general public have typically turned to the U.S. Department of Energy’s Energy Information Administration (EIA), which every year publishes its Annual Energy Outlook (AEO).

In Drilling Deeper, PCI Fellow David Hughes took a hard look at the EIA’s AEO2014 and found that its projections for future production and prices suffered from a worrisome level of optimism. This lead us and others to raise important questions about the wisdom of some energy policies and infrastructure projects (for example, the approval of Liquified Natural Gas export terminals and the lifting of the crude oil export ban) that have been pursued largely on the basis of the EIA’s rosy forecasts. Recently, the EIA released its Annual Energy Outlook 2015 and so we asked David Hughes to see how the EIA’s projections and assumptions have changed over the last year, and to assess the AEO2015 against both Drilling Deeper and up-to-date production data from key shale gas and tight oil plays. What follows are Hughes’s findings regarding shale gas. The AEO2015’s tight oil projections will be reviewed in early September 2015. Read PCI conclusions here

11 August 2015, The Conversation, What does Australia’s new 2030 climate target mean for the local coal industry? Australian Prime Minister Tony Abbott has promised that his government’s new 2030 climate target will be good for the environment, good for jobs and good for protecting the nation’s coal industry. After announcing Australia would reduce greenhouse gas emissions by 26-28% below 2005 levels by 2030, the prime minister was asked about what impact that could have on the local coal industry. He replied:

We are not assuming a massive close-down of coal. In fact, one of the things that will benefit the world in the years and decades to come is if there is a greater use of Australian coal, because high-quality Australian coal as opposed to low-quality local coal is going to help other countries to, if not reduce their emissions, certainly reduce their emissions intensity. One of the reasons why China is forecast to substantially reduce its intensity, if not its overall emissions, is because it is forecast to rely increasingly on coal from countries such as Australia…We certainly aren’t forecasting the demise of coal. Our policy doesn’t depend upon the demise of coal. In fact, the only way to protect the coal industry is to go with the sorts of policies that we have. That’s why I think our policies are not only good for the environment but very good for jobs.

Australia currently gets three-quarters of its electricity from burning coal – but most of the nation’s coal production, particularly from New South Wales and Queensland mines, is for global exports. The Conversation asked a panel of energy experts for their forecasts for Australian coal in the light of the 2030 target and the upcoming climate talks in Paris. (You can also read why experts have warned Australia’s post-2020 climate target isn’t enough to stop 2C warming.) Read More here

23 June 2015, Climate Council’s new report reveals that if all of the Galilee Basin coal was burned, an estimated 705 million tonnes of CO2 would be released each year – more than 1.3 times Australia’s current annual emissions. Tackling climate change effectively means that existing coal mines will need to be retired before they are exploited fully and new mines cannot be built. This is particularly relevant for Australia as plans are on the table to open up the Galilee Basin, and expand coal mining operations in the NSW Upper Hunter Valley and in the Liverpool Plains, a region described as the food bowl of Australia. Moving away from fossil fuels means that new energy sources, like solar and wind, must come online rapidly. Click on image to access report:

16 June 2015, The Conversation, Talk of the demise of Australian coal production is largely political, not economic. The problem for the countries that presently mine and burn coal is that there are currently few low cost alternatives. Most countries in the world today are focused on trying to ensure their citizens have access to electrical power. This is difficult without low cost base load electricity production and at present, coal provides an affordable solution. As at the end of 2012 there were 75 countries producing coal. These countries ranged from Nepal with production of 17,640 short tons in 2012, through to China with production of 4.017 billion tonnes in the same year. It’s worth noting that Australia was ranked 5th (after China, the United States, India and Indonesia) with coal production of 463 million tonnes in 2012. While these rankings move around a little over time there is no doubt Australia is still a major player in the market for coal.

Regional coal production

U.S. Energy Information Administration (EIA) U.S. Energy Information Administration (EIA)

If you focus on regional coal production since 1980 (see chart above), it is clear production in most regions is levelling out or falling except for Asia and Oceania. When you break this group down there are four major producers involved: China, India, Indonesia and Australia, with a large number of other countries producing considerably less. This is evident in the chart below. Coal production has increased in each of these countries since 1980 though the rate of increase since 2000 is greatest for China.

Coal production by China, India, Indonesia and Australia

While Australia’s coal production is important, it is not the largest coal producer. There are a number other countries in the world that produce very large amounts of coal. If Australia were to cease production of its coal there would be an initial increase in world prices. Nevertheless, it is expected that other producers would fill the gap, particularly given the more recent falls in demand for coal. Read More here

Map of existing and potential carbon pricing schemes. Source: World Bank Carbon Pricing Watch 2015

Comparison

- The report says in 2015, carbon pricing covered around 12% of the world’s emissions.

- The actual volume of carbon that was covered by a carbon price in 2015 rose slightly from the previous year, from almost 6 gigatonnes of carbon dioxide equivalent up to 7 gigatonnes, the World Bank report says.

- Over the last decade, the picture has changed more dramatically, as the graph below shows. In 2005, only 4% of the world’s annual greenhouse gas emissions were priced, and almost all of this was a result of the EU’s newly launched emissions trading system (EU ETS). Read More here